Built-In Strategies

Beating the market couldn't be easier with the Research Wizard. The program comes loaded with more than 50 of our most successful stock picking strategies. These strategies have performed in both up markets, down markets, and everything in between.

The key to success is in knowing what works, and then doing what works. Pick and choose the strategies that fit your trading style. Then just point and click and get your list of the highest probability stocks that make money.

Zacks Stock Strategies

vs. S&P 500

Average Compounded

Gains Per Year

2000 - 2025

These backtested retuns assume weekly rebalancing except that R² Growth rebalances every 4 weeks, Growth & Income Winners every 12 weeks.

For more information on the performance numbers displayed visit www.zacks.com/performance.

S&P 500 is owned and published by McGraw-Hill

Screening

The Research Wizard is easy to use for both the beginner and experienced investor. You can use our built-in strategies or create your own. Screen with more than 650 different fundamental data items on over 10,000 stocks. And create an unlimited number of customized items and calculations in our 'Calculation Expression' feature. Virtually anything you want to look for, you can ask the Research Wizard to find and have your answer within seconds. Then once your screens and reports are created, they can be saved for 'one-click' access the next time.

Your stock-picking results are displayed in an easy-to-read format which can quickly and easily be sorted according to your preferences. Or you can export your results to other applications such as Excel.

Learn more about this powerful stock screener

Success in trading begins with finding the right stocks to buy and sell.

That means having a fast and reliable way for picking winning stocks that meet certain characteristics, with the most profitable opportunities to make money.

Most people underperform in their portfolios because their universe of familiar stocks is relatively small, and this limits their ability of getting into better ones.

Unfortunately, too many people get their stock picks simply because they were talked about on TV, touted on the internet, or written about in the newspaper (not to mention tips from a friend). But these are not reliable ways to find the best stocks.

And with so many stocks out there, you need a way to find the good ones.

So if you want to find stocks that meet certain characteristics, you can do so quickly and easily with a stock screener.

There are plenty of screeners out there. But they are not all created equal. And your ability to find winning stocks can depend on how capable your stock screener is.

For example, we’ve all heard people say that when they golf with a better golfer it raises their game. And that's true for any sport. Or when they work with a talented co-worker it makes them perform better.

The same is true for the tools that you use. So it’s important you have the right tools for the job.

Most screeners will cover the basics. For example, most every screener will have a P/E ratio. But do they have P/E ratios using EPS Actuals, and P/E ratios using F1 Estimates? Both of those are needed to calculate a Price Target. What about P/E ratios using the Forward Twelve Month Estimates, or the P/E ratios' average over the last 5 years, or the high and low P/E ratios over a certain period of time?

What about the PEG ratio? Or the Price to Book ratio? Or the Price to Cash Flow? Or the Price to Sales ratio? These are important valuation metrics to have.

The Research Wizard's main screening window has all of the Categories and Items (all 650+ of them) smartly organized with plain language descriptions for easy selection. (See below.)

Just point and click and start picking better stocks.

Another major difference between stock screeners are the operators, e.g., the greater than sign (>), the less than sign (<), the equal to sign (=), etc. All screeners have the basics. But most stop there.

The more sophisticated ones will also include ways to define ranges (inclusionary and exclusionary), finding the top or bottom values in a set (#'s or %'s), or apply the criteria to a Sector or Industry or to the whole of the market itself, and even search more specifically within a user defined group to find the best stocks within them.

Operators are the defining rules with how you interact with the data items. Get the most out of your screening with all of the different operators available in the Research Wizard.

In addition to the hundreds of different data items, and the vast selection of operators, the Research Wizard also lets you create your own customized items in the Calculation Expression feature.

This lets you compare one item to another item, combine different items together, even compare an item's value to its value from a different time period.

This gives you extraordinary flexibility to create any item or idea you may have and helps you pinpoint exactly what you're looking for.

Once you've created a few customized items you'll find yourself using them again and again to produce virtually any kind of data you can imagine, helping you zero in on just the right stocks.

But the best part of the Research Wizard is that it's fast and easy to use.

Let's face it, if something is difficult or time consuming, you're likely to put it off or not do it. That's fine if the task is cleaning your garage. Not so much if the task at hand is managing your portfolio.

A smart interface that's easy to use is important to keep you coming back. And you'll realize just how fun picking better stocks can be.

Backtesting

With backtesting you can know definitively how effective your stock-picking strategies are BEFORE you place your next trade. No more guesswork. And no more trial and error. Know for certain if your strategy picks stocks that go up or go down. This can have a huge impact on the performance of your portfolio.

The Research Wizard tests your strategy and gives you its historical performance. This includes a summary of your strategy, a comparison to the S&P (or the Dow or Nasdaq), the number of stocks traded, along with the individual returns of what stocks were bought and sold in the past. See the winning percentage of your holding periods, its max drawdown, and how your investment strategy performed in both up and down markets.

And every test automatically shows your strategy’s equity curve (performance chart) so you can quickly and easily see how profitable your screens really are. If you’re not backtesting, you’re just guessing.

Learn more about Backtesting

Screening for stocks is the first step to becoming a successful trader. But just because you narrow down 10,000 stocks to only a handful, doesn't mean you've picked the best stocks on the planet. You might have picked the worst ones.

But how will you know? Backtesting!

Once you've created a screen, you can see how successful that strategy has performed in the past, so you'll have a better idea as to what your probability of success will be now and in the future.

Of course, past performance is no guarantee of future results, but what else do you have to go by?

Think about it. If you saw a that a stock-picking strategy did nothing but lose money year after year, trade after trade, stock after stock, over and over again, there's no way you'd want to use that screen to pick stocks with. Why? Because it's proven to pick bad stocks. Sure, it might start picking winners all of a sudden, but it may also continue to pick losing stocks the way it always has.

On the other hand, what if you saw that a screening strategy did great year after year, period after period, over and over again? You'd, of course, want to use that strategy to pick stocks with. Why? Because it's proven to pick profitable stocks. And while it may start picking losers all of a sudden (now that you're using it, right?), it may also continue to pick winning stocks just like it had been doing over and over before.

Just because you have a great strategy for picking winning stocks, it's not going to preclude you from ever having another losing trade. On the contrary, even some of the best strategies 'only' have win ratios of 60%, 70%, or even 80% -- not 100%.

But if your stock-picking strategy picks winners far more often than it picks losers, you can trade your strategy with confidence knowing you have the highest probability of your next trade being a winner.

Note: Backtesting has its limitations. To learn more about potential limitations and biases in backtesting please visit www.zacks.com/performance.

After you've selected the screen you want to test (for this illustration, let's look at the Filtered Zacks Rank 5 strategy), then determine the holding period you want to apply to it (we'll use a 1-week holding period, but you can choose between a 1-week, 2-week, 4-week, 12-week, and 24-week holding period), the time span you want to run your test over (for this example, we'll do it over 2016), and the benchmark you want to compare it to (we'll compare it to the S&P 500), you're ready to run your test.

Once the backtest is finished, your backtest report is ready to view.

No more hemming and hawing, or wondering if you're screening strategy is a profitable one or not. Now you're in the know.

The first thing you'll notice in the backtest report is the performance chart. This will instantly show you how the strategy has performed and if your strategy is worth looking into any further. Clearly, this one looks pretty good.

You can also display the information as a bar chart (not shown) rather than a line chart.

The rest of the report is broken down into two sections: the main backtest report and the statistics table.

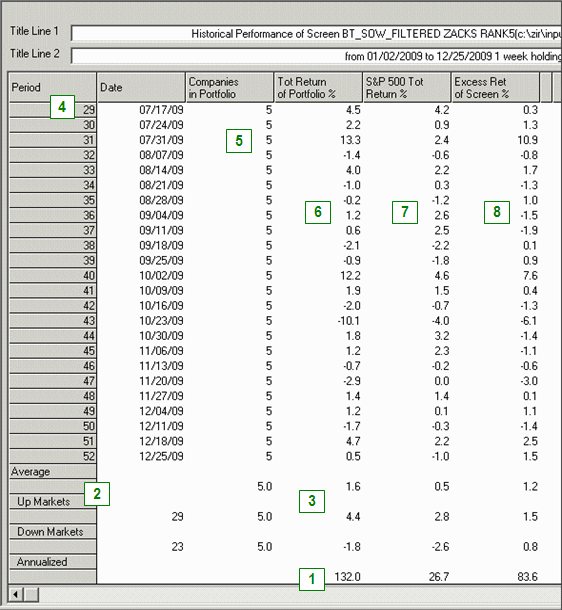

The screenshot shows the first six columns of the main backtest report. Let's take a closer look at what's in each of these sections.

Displays the annualized returns for your backtest report.

Indicates the number of up and down markets (periods) seen by the market, i.e., the benchmark selected – in this case the S&P 500 - during your test period.

In this example, there were 29 one-week periods where the S&P was up. And 23 one-week periods where the S&P was down. This will show you if your test period was predominantly bullish or predominantly bearish.

(Of course, the benchmark's returns will show you how bullish or bearish the market was as well. But the more granular view broken down by periods also provides some very useful information.)

Specifies the average return of your strategy and the benchmark during your test period, including the average return when the market was up and the average return when the market was down. It also includes other summary statistics such as the average number of stocks held and more.

Lists the individual holding periods in your test along with the corresponding start dates.

Specifies the number of stocks that passed your screen in each period. In this example, this screen was designed to always pick five stocks. But if the screen generated different amounts of stocks in different periods, it would display that as well as provide an average at the bottom.

Displays the strategy's periodic returns.

For example: in Period 29, this shows that had you run the screen at that time, 5 stocks would have qualified your screen. Had you bought all of those stocks in an equal dollar weighted manner and held onto those stocks for the duration of the holding period (in this case, 1 week), the portfolio would've increased by 4.5%.

Indicates the benchmark's periodic returns.

The S&P during that same period would've gained 4.2%.

Lists the excess returns (or deficit returns) of the strategy compared to the benchmark.

This shows the strategy outperformed the S&P by 0.3% during that period.

The next section of the report is the statistics table. This displays the return and risk metrics.

The table includes:

Total Compounded Return % – performance for the test period.

Compounded Annual Growth Rate % – a measure that translates performance into a yearly return.

If the test period is for an entire year (like this is one is), the Total Compounded Return and the Compounded Annual Growth Rate will be the same.

If the test period was for more than a year (five years for example), or less than a year (5 months for example) the Compounded Annual Growth Rate would show the annual return (i.e., how the 5-year total return breaks down into annual returns or how the 5 month return would look on an annual basis if the same type of results continued for the rest of the year).

Win Ratio – winning periods divided by the total number of periods in the test. (This shows how often your strategy’s portfolio wins and how often it loses.)

Winning Periods/Total Periods – number of winning periods out of the total number of periods in the test.

Avg. # of Stocks Held – average number of stocks held in the portfolio each period.

Avg. Periodic Turnover % - percentage of turnover (stocks sold and new stocks bought) in the portfolio each period. For example, if the portfolio held an average of 6 stocks each period and you replaced an average of 3 stocks each period (sold 3 stocks for 3 new ones), the Turnover % would be 50%.

In this example, the Periodic Turnover is 54.9%.

This is a good time to point out that just because you're rebalancing your portfolio every week does not necessarily mean you're turning over your entire portfolio every week. The weekly rebalance simply means that it's checking the criteria each week (running the screen each week) to see what stocks qualify. If the stocks from last period still qualify, you'll hang onto those stocks for another period. If they no longer qualify, you'll sell those stocks and replace them with the new stocks that qualify for that period.

Avg. Return per Period % - average return for the portfolio on a periodic basis.

Avg. Winning Period % and Avg. Losing Period % - average win or loss on a periodic basis.

Largest Winning Period % and Largest Losing Period % – largest win or loss in a single period.

Max Drawdown % – the maximum drawdown, i.e., the largest drawdown in equity from a historical peak.

This can be a single period or a series of losing periods (and not necessarily in a row). To further define it, it's the largest equity pullback from a previous equity peak. In short, it measures how much an investor might have seen his equity drop by if he had traded the strategy during that time period. This could mean a drop in profit or a drop in starting equity depending on when you began.

If in one period the strategy was -3%, and the next period the strategy was -3%, that's a total of -6%.

If the strategy then gained 2%, the total is now only -4%. (And the Maximum Drawdown at this point would be recorded as -6% since that was the largest pullback up to that time.)

But, if the next period was -3%, and the strategy then hit a winning streak, the Max Drawdown would be recorded as -7%.

Final Calculation: -3% plus -3% plus 2% plus -3% = -7% total. And that would be your Max Drawdown.

(The exact number would be slightly different than this simple illustration as a 2% increase from a lower level would not completely erase a 2% decrease from a higher level. But the illustration (aside from a tenth of a percent) was to show that the losses do not need to be in a row to determine the maximum drawdown.)

This is a good statistic to know so you can decide whether or not this risk level is an acceptable risk level for your trading.

In the above example, the Max Drawdown is -21.9%. The S&P's was -26.3%

Other good risk measurements are:

Average Winning Stretch (# of Periods)

Average Losing Stretch (# of Periods) along with the Best Stretch (# of Periods) and the Worst Stretch (# of Periods)

These measurements illustrate the number of consecutive Winning Periods or Losing Periods.

Note that these measurements are helpful in identifying the patterns of winning periods and losing periods. If your strategy happens to go through a losing period, you can see the historical 'norm' and the probability of success for the next period or periods.

You can also view the backtest period details for each period. By selecting one of the periods, you can call up a Backtest Period Details window.

In this window, you can see which stocks qualified in each historical period as well as how the stocks performed individually.

Also, by clicking on any one of the tickers, it'll show you how often that stock came thru your screen during the test period and if any of them were in consecutive periods.

This kind of detailed insight gives the user extra confidence to feel comfortable with a strategy and if it's right for him.

The Backtest Period Details window can be displayed for each period separately, or you can pull up a Details window with all of the periods in it.

By selecting the Annualized Return Number in the main Backtest Report, you can call up a Backtest Period Details window with all of the periods displayed.

And of course you can export all of this data to Excel as well.

Virtually everything you want and need to know about your stock-picking strategy is now right at your fingertips.

Seeing how good or bad a strategy has performed in the past is an invaluable insight. No more suffering through time-consuming trial and error, or costly mistakes.

Know what your probability of success is before your next trade.

Advanced Backtesting

For advanced users, you can run automated backtesting routines to verify a model's robustness. Perform ‘best case/worst case' analysis studies. Do optimum valuation testing to determine the most profitable parameters of a screen. Narrow that down even further to determine the most optimum valuation ranges for a particular item. And run multi-strategy backtests on an entire portfolio of strategies (screen of screens) to see how they act together.

You won't find this in any other backtester. But it's all here in the Research Wizard. This changes everything.

Learn more about Advanced Backtesting

Testing your strategies over many different time periods is critical to making sure your strategies are robust enough to make money in all markets no matter when you start using it.

When you're rebalancing your strategies once a week, you'll essentially be participating in every week it picks new stocks. But what if you're using a 2-week holding period or a 4-week holding period, etc.?

If your strategy, for example, is to buy stocks at the beginning of each month and hang onto them for the remainder of the month, it would be a good idea to see what would happen if you picked your stocks in the second week of the month, or the third week, or the fourth.

This is important because depending on when you run your screen, your strategy could pick a different list of stocks. The list might be slightly different (or meaningfully different) each week you run your screen. And these different lists will then be held over different sets of four-week periods.

Therefore, if your strategies do well no matter what and when, you know you've got something special -- a proven, profitable and repeatable way to pick winning stocks.

Much of this can be done individually through just regular backtesting. But the automated robustness check saves time by allowing you to test your strategy over multiple start dates with only one click of the mouse.

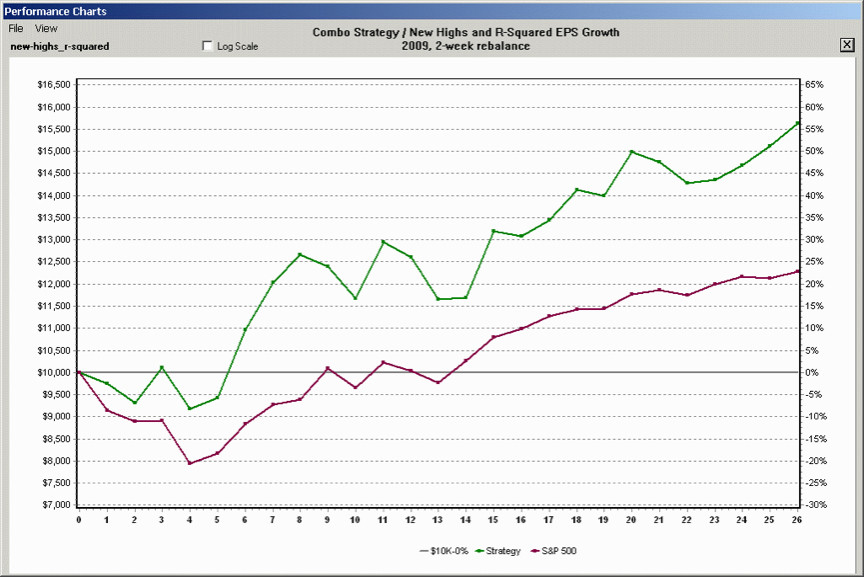

Let's take a look at one of the strategies we rebalanced using a 4-week period to see how this can help your screen analysis. For this example, we'll use the R-Squared EPS Growth Rate.

The performance chart will look different in that it now shows several more performance lines on it. Each line represents a different start date with one of the lines showing the average performance of the combined start dates.

In the first chart, the performance lines are all relatively close together. This means the performance of this particular strategy is pretty robust. Regardless of which date it was started on (the first week of the month, or the second week of the month, or the third week or the fourth – there are four possible start dates in a four-week holding period), the results were largely the same. And ideally, that’s what you'd want to see.

If you change the setting on the chart, you can change the view from all of the runs (which includes the average run), to a chart with only the average run displayed (as shown on the second chart).

You can also change the view with only the four start dates displayed (as shown on the third chart).

Whatever performance run you're interested in, viewing it can be done with a simple click of the mouse.

You can also analyze your strategy through the main backtest report that's generated. Like the standard backtest report, it'll give you a breakdown of all of the stocks in all of the periods, run by run so you can see how they performed.

But in this statistics table, it also provides a performance summary of the average runs along with the best and worst runs as well.

Here you can see the average compounded annual growth rate was 24.9%. Additionally, it shows the best run (Run 2) being 27.0% and the worst run (Run 1) being 22.7%.

And it'll do the same for the maximum drawdown as well. As you can see the average maximum drawdown was -34.2% in comparison to the markets -50.6%. The largest maximum drawdown (Run 1) was -42.8%. And the smallest maximum drawdown (Run 2) was -23.9%.

For this example, you can see that regardless of when you start it, the returns look meaningfully the same with approximately the same drawdowns.

The more you know about your strategy, the more informed trading decisions you can make.

Combo backtesting lets you test multiple strategies together which is perfect for incorporating different screening strategies into one portfolio. By testing different strategies together in your portfolio, you can see how they would do as a whole.

This kind of backtesting is different than putting all of your parameters together into one screen. The parameters for a Deep Value screen, for example, and the parameters for an Aggressive Growth screen would likely cancel each other out if put into one big screen, leaving you with no stocks coming through at all. But if you backtested a portfolio of screens, you'd now see how these different screening styles could complement each other in the grand scheme of a fleshed out portfolio.

In this chart, it shows how two different strategies (the New Highs momentum screen and the R-Squared value screen) look together in the same portfolio.

The chart will display the combined performance line, i.e., how the New Highs strategy and R-Squared strategy performed together as a portfolio. It will also produce a backtest report complete with a statistics table showing you the profit and loss profile together.

But you can change the chart setting to show you how the individual strategies performed on their own (as shown in this chart).

Now you can see how each individual strategy has performed separately and how they contributed to this combo strategy.

In this example, you can see that the R-Squared Growth Rate strategy (orange line) started the year off better than the market and better than the New Highs strategy (blue line). By the middle of the year, the R-Squared started to flatten out while the New Highs started to kick into gear. Then as the year was winding down, the New Highs started to pull back while the R-Squared accelerated to the upside. While one style was underperforming, the other was picking up the slack. But together (see previous chart) they created a smoother equity curve as one complemented the other.

You can also use the Combo Strategy backtester in other ways. Instead of seeing how well multiple strategies work together as whole, you can pit one against the other to see how they compare.

In the example above, it shows the performance of the top 50% of Zacks Ranked Industries (blue line) vs. the bottom 50% of Zacks Ranked Industries (orange line). This chart instantly shows how these screens performed and the magnitude of the difference over the entire length of time.

Seeing a chart with one screen overlayed on top of the other can oftentimes provide a more meaningful observation than looking at them one by one or just looking at the numbers and data.

You can also do Optimum Valuation testing to see what the most profitable valuation range is for any given item.

This eliminates a lot of trial and error when building a new strategy. By testing which valuation ranges produce the best results, you can start applying those values to your screens instead of guessing what might work best.

In this example to the right, we have a combo screen with six different individual screens inside, each with a different P/E range: 0-10, 10-20, 20-30, 30-40, 40-50 and greater than 50.

By running the Combo backtest, you can instantly see which valuation ranges work the best. In this example, you can see the P/E ratio of 0-10 (blue line) works the best.

And this type of testing can be done on virtually any kind of item.

We've all heard the old adage: knowledge is power. It's a great saying because it’s true. And that saying couldn't be truer than when it comes to investing.

There's no better way to improve your trading than to know what works and what doesn't before you get into the market.

Screening and backtesting is fun if you're getting results. And the more screening and backtesting you do, the more profitable you'll become.

For more information view our Advanced Backtesting Video

Stocks and Portfolio Ranking

Picking good stocks for your portfolio is one thing, but it's also important to monitor your stocks' attractiveness. With Hot Maps, you can graphically evaluate the attractiveness of the stocks in your portfolio, and evaluate the stocks from your screening lists. In the Hot Maps feature, stocks are ranked as colors (shades of green for the best to shades of red for the worst) to quickly spot the best and the worst companies without any guesswork.

There's also a Scatter Plot that allows you to plot the linear regression of any selected variables. Analyzing stocks, comparing tickers and managing your portfolio has never been easier.

Price and Fundamental Charts

The Research Wizard can visually display virtually any type of fundamental data you're interested in. With a click of a button you can flip through standard Price charts, EPS Consensus charts, Broker Recommendation charts and more. This also includes the hundreds of different data items within the program. Now you can chart your stock's Sales, Earnings, ROE, Net Margin, Projected EPS, P/E, Cash Flow, etc. (and literally hundreds more), and see how your stock responds to the item's changing values over time. Chart one item at a time, or layer as many different items on a chart as you wish.

And it doesn't stop there. You can chart the fundamentals of an individual stock, or all of its peers, or the industry and sector itself. Access this data going back 20 years (and counting), and visually see how your item of interest has trended over time and how it correlates to the stock's price movement. No more staring at mind-numbing spreadsheets or reams of data. See your data graphically visualized so you can make smarter decisions in less time.

Plus, Formulas for Finding Them on Your Own

Try our Research Wizard stock-selection program for 2 weeks to access live picks from our proven strategies, modify existing screens, or test and create your own at the touch of a button. Absolutely free and no credit card needed.